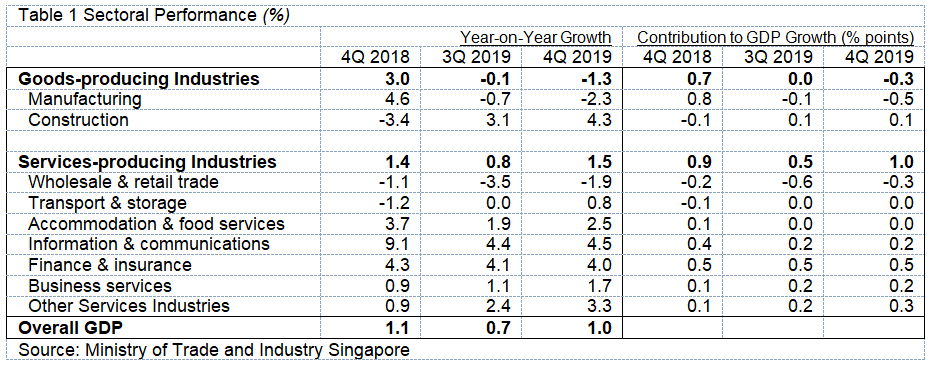

In 4Q 2019, Singapore’s economy grew by 1.0%, year-on-year, improving slightly from the 0.7% expansion in the previous quarter – see table 1. The finance & insurance, other services industries and business services sectors were the largest contributors to GDP growth. On a quarter-on-quarter seasonally-adjusted annualised basis, Singapore’s economy expanded by 0.6%, which is a decline from the 2.2% growth in the preceding quarter. For the whole of 2019, Singapore’s economy grew by 0.7% on a year-on-year basis.

In 2019, the contraction in output from the goods-producing industries (-0.8%) was attributed to a contraction in the manufacturing sector (-1.4%). The fall was mainly driven by declines in output in the electronics, chemicals, precision engineering and transport engineering clusters. On the other hand, the construction sector increased 2.8% due to growth in both public and private sector construction activities.

The services-producing industries continued to expand (1.1%), albeit at a slower pace. The information & communications sector recorded the highest growth rate (4.3%), followed by the finance & insurance sector (4.1%).

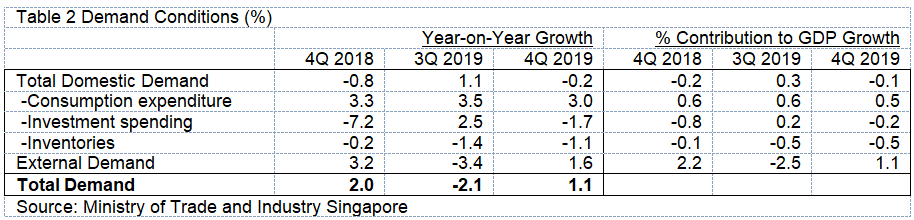

Demand Conditions

In 4Q 2019, total demand rose by 1.1%, year-on-year, reversing the 2.1% decline in 3Q 2019. Domestic demand declined slightly while external demand recovered – see table 2. For the whole of 2019, total demand fell by 0.7%, a sharp decline compared with the 6.3% growth recorded in 2018.

Labour Market and Productivity

In 4Q 2019, total employment increased by 18,300, quarter-on-quarter, smaller than the increase of 26,000 in 3Q 2019, but it was higher than the increase of 15,900 in 4Q 2018. Employment growth was driven by increases in employment for all sectors, with the services sector registering a gain of 13,000, construction up by 4,600, and manufacturing up by 700.

Year-on-year, labour productivity fell by 1.6% in 4Q 2019, larger than the 0.9% fall in 3Q 2019. Productivity of outward-oriented and domestic-oriented sectors respectively fell by 2.3% and 0.6%. For the whole of 2019, labour productivity decreased by 1.5%, a reversal from the 3.9% growth in 2018. By sector, only the construction and finance & insurance sectors experienced growth, while all other sectors suffered a decline in productivity

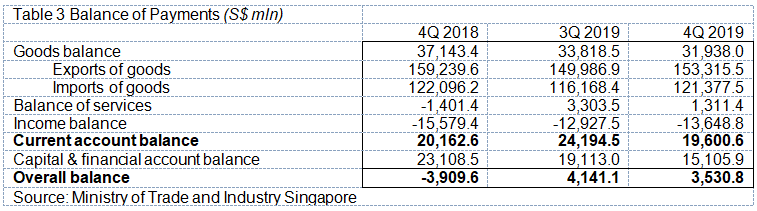

Balance of Payments

Singapore recorded a balance of payments deficit of S$11.4 bln in 2019, declining from the surplus of S$16.9 bln in 2018. This was due to a larger net outflow from the capital and financial account which outweighed the current account surplus. In 4Q 2019, the balance of payments recorded a surplus of S$3.5 bln, which narrowed from the surplus of S$4.1 bln in 3Q 2019 – see table 3.

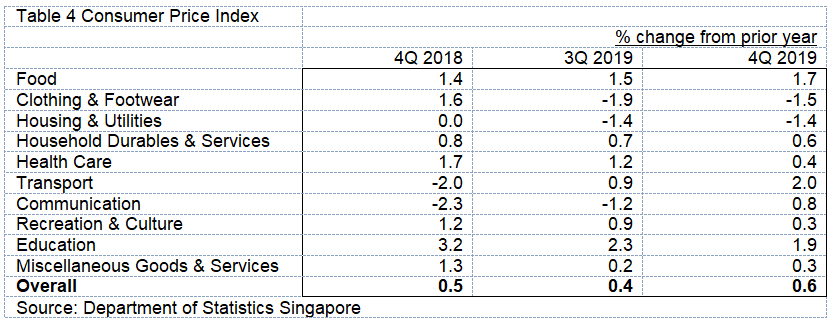

Price, Interest, and Exchange Rates

Year-on-year, the consumer price index (CPI) increased by 0.6% in 4Q 2019, up from the increase of 0.4% in the previous quarter – see table 4. For the whole of 2019, the CPI rose by 0.6% with the largest contributor to inflation being the food category.

At the end of 4Q 2019, the prime lending rate declined to 5.25%, from 5.33% in the same period a year ago. In terms of the average interest rates quoted by the 10 leading banks, the 12-month fixed deposit rate rose by 0.12 percentage points to 0.57%, while the savings deposit rate remained unchanged at 0.16%.

In the foreign exchange market, at the end of 4Q 2019 the Singapore Dollar appreciated against the Euro, US Dollar, Australian Dollar, Chinese Renminbi, Hong Kong Dollar and Malaysian Ringgit by 3.5%, 1.3%, 2.1%, 2.7%, 0.7% and 0.2% respectively compared with a year ago. On the other hand, it depreciated against the British Pound and the Japanese Yen by 2.1% and 0.3% respectively.

Comments

Although Singapore’s economic growth improved slightly in 4Q 2019, it is expected to be subdued in 2020. The COVID-19 has disrupted global supply chains, discouraged international trade and tourism. While the US-China trade war may have reached a truce, it could flare up anytime, depending on the mood of US politicians. Besides that, many global risks remained unresolved, including Brexit and recessionary risk in a low interest rate environment. Singapore, being a small open economy, is extremely vulnerable to the adverse global developments, especially when it involves China, the biggest contributor to world economic growth and Singapore’s largest export market and tourist generating country.

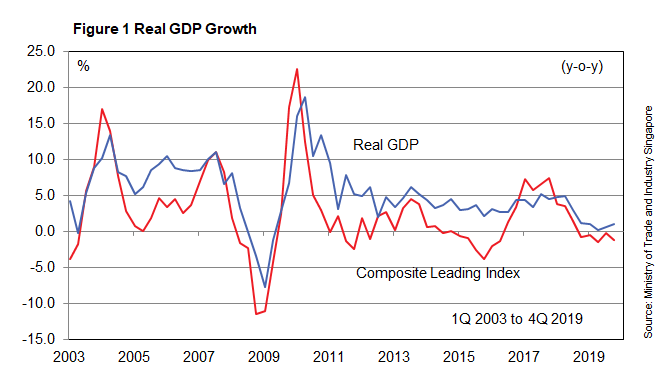

Reflecting the dire conditions, the composite leading index (CLI) fell 1.2%, year-on-year, in 4Q 2019 – see figure 1. The CLI has been declining since 4Q 2018. As a result, i Capital expects Singapore’s real GDP to fall in the range of 0.2% – 1.3%, year-on-year, in 1Q 2020. For the whole of 2019, economic growth is expected to be in the range of -1.2% – 0.5%.