Global warming and an ultra-loose monetary policy are some of the changes that the global community has been suffering from. The former ever since the UK, Europe, and the United States began industrializing 200 to 250 years ago; the latter ever since the same bunch of countries, led by the US, created the 2008 global financial crisis.

Shockingly, the United States, the UK, and Europe are still behaving as if they are on a moral high horse, lecturing the rest of the world on what is right and how to behave. Looking back, it is amazing how little the world has changed. How these countries with their irresponsible and self-interested leaders continue to behave with reckless selfishness and let the rest of the world suffer. Leaders like Tariff Trump, Scott Morrison of Australia and now Boorish Johnson of Britain behave as if the world has merely stood still for the last 200 to 250 years.

In this new volume 31 of i Capital, we continue to reflect on the state of the nation and the state of the world and share our thoughts on disruptions, technological changes, and changes in investing, economy and society. We have written about climate change and its irreversible trends; last week, we focused on the irresponsible ultra-loose monetary policies of the US, Japan, Europe and more, brought about by the colossal mistakes made by the central banks in the US, the UK, and Europe. This issue, as we focus on another fundamental shift, we turn our attention to another key aspect of macro-economics: fiscal policy, especially of the key economies.

Looking back at fiscal policy over the last century, it is remarkable how so much has changed, especially since the 1930 Great Depression. First, a primer on what fiscal policy is.

Fiscal policy refers to government revenue and spending; it refers to a government's policy regarding what the public sector will spend and how the public sector will finance this spending, which is typically financed through taxes and debts. How does fiscal policy work ? If a government wants to stimulate growth in the economy, it will increase public sector spending for goods and services. This will increase demand for goods and services and as production goes up, companies and maybe even the public sector itself will hire more people. People that were once unemployed may now have jobs and money to spend on goods and services. Consequently, an expansionary fiscal policy via more government spending tends to boost economic growth. The same result can also be achieved by changing the economy’s tax structure – it can lower tax rates, implement a new tax structure or launch tax incentives, all of which are aimed at boosting consumer and/or investment spending and eventually economic growth. An expansionary fiscal policy will typically lead to budget deficits.

On the other hand, if the government thinks that the economy is overheating, that it has borrowed too much or that the public sector has become too big, the government may implement a contractionary fiscal policy either by decreasing government spending and/or increasing taxes. This can be done with or without a tight monetary policy. Businesses will slow production, resulting in less hiring and investment. A contractionary fiscal policy will decrease overall demand in an economy. Since 2008, the countries which have adopted a contractionary fiscal policy are those from Europe, which lived beyond their means before 2008 – nowadays they are called austerity measures. A contractionary fiscal policy will typically lead to narrower budget deficits or possibly even budget surplus. This brings us to how much the world has changed, at least on the surface.

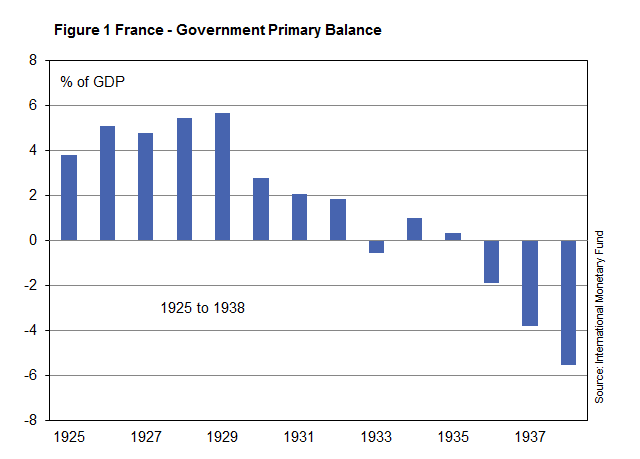

In the era before the 1930 Great Depression, the prevailing economic wisdom taught was that it was good for governments to run budget surplus. A look at France before and after the 1930 Great Depression exemplifies this mind-set (figure 1).

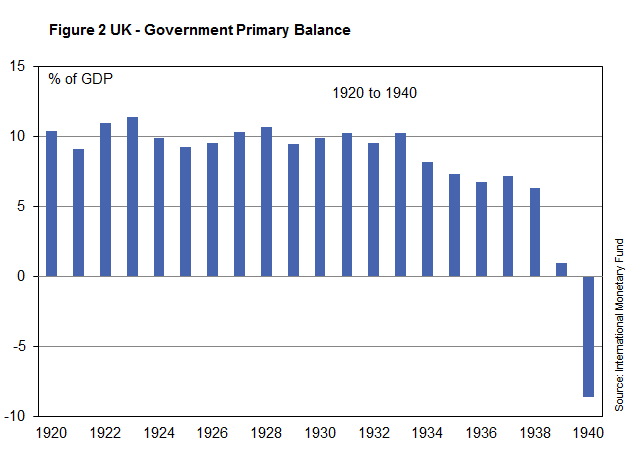

In the same period, the experience of the UK was even more extreme (figure 2). The General Theory of Employment, Interest and Money written by JM Keynes, which created a profound shift in economic thought, was only published in 1936. It provided theoretical support for government spending and budgetary deficits. Keynes denied that an economy would automatically adjust to provide full employment even in equilibrium, and believed that the volatile psychology of markets and people would lead to periodic booms and crises.

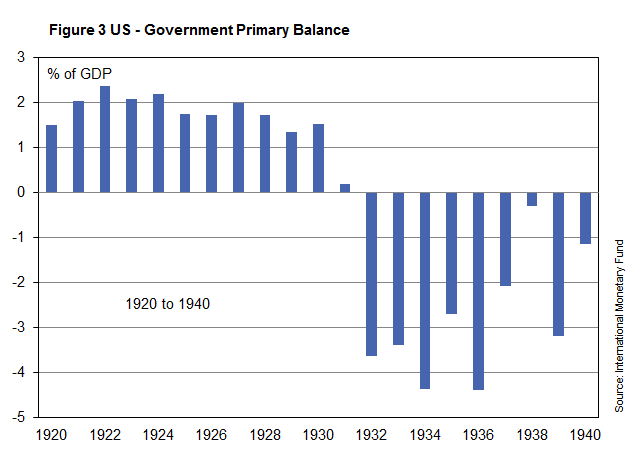

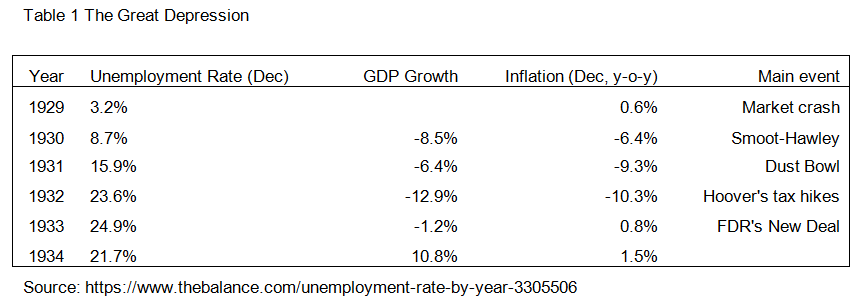

The same economic thinking prevailed in the US before the 1930 Great Depression hit it hard (figure 3). The prevailing assumption was that budget surplus was good and needed to be maintained at all times. This policy approach was adopted even when the recession was slamming the US economy in the initial period of the Great Depression.

President Herbert Hoover even asked for a temporary tax increase. In Jun 1932, he raised the top income tax rate from 25% to 63% and quadrupled the lowest tax rate from 1.1% to 4%. In fact, Hoover was imitating policies in Britain and Germany, where big tax hikes had already been implemented. With US unemployment rate hitting 25% and the whole US economy in deflation, Hoover easily lost his place to Roosevelt (Table 1).

In response to the severe crisis and in a fit of total desperation, Franklin Roosevelt launched the New Deal in three waves from 1933 to 1939 and made use of US government spending to tackle the economic crisis at that time. Budget deficit via an expansionary fiscal policy became the new orthodoxy. The US economy stabilised (table 1).

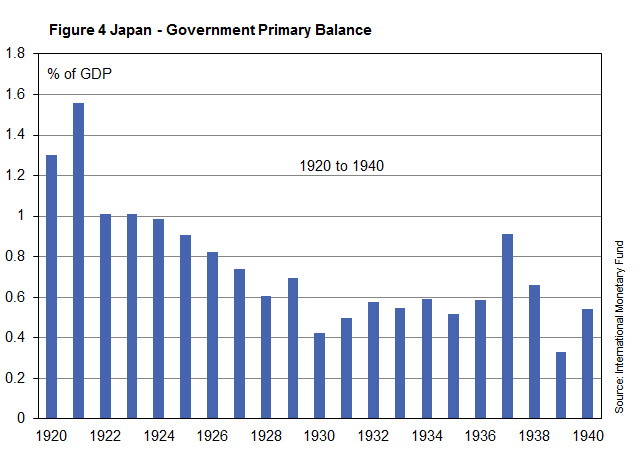

Japan had the same conservative fiscal approach (figure 4). Unlike modern day Japan, she maintained a budget surplus throughout the 1930 Great Depression. This was in part due to the fact that the Japanese economy was not as severely hit as those of Britain, Europe or the United States. Why was this the case ?

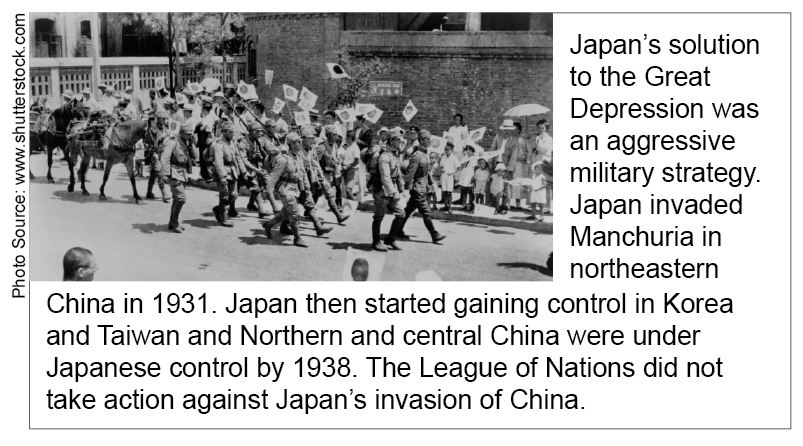

Initially, Japan was not spared either. From 1929 to 1931, Japan’s economy shrank by 8% and the value of Japanese exports plunged 50% between 1929 and 1931. Japan’s violent solution was an aggressive military strategy and she began to invade other countries. Japan’s military invaded Manchuria in Northeastern China in 1931. Japan then started gaining control in Korea and Taiwan. The League of Nations did not take action against Japan's invasion of China. In 1933, Japan withdrew from the League. Japan continued to invade China, easily crushing all opposition. Northern and central China were under Japanese control by 1938. Japan’s economy recovered not through an expansionary fiscal policy but through brutal and implacable military expansion.

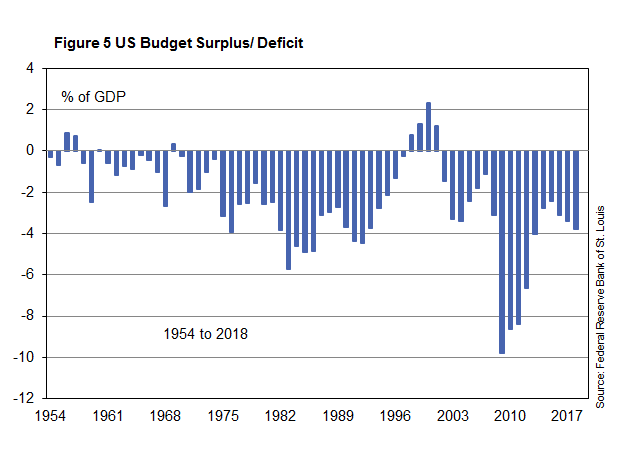

Since the Great Depression and the 2008 US-led global financial crisis, all the advanced economies have maintained an expansionary fiscal policy, even though this has meant persistent and high budget deficits. The experience of the United States typifies this new thinking, which essentially admits and recognises the importance of the role of government in the economy. Unlike the days before 1930, the United States has been experiencing a budget deficit for decades, except for a few years under president Clinton (figure 5). The US budget deficit immediately after 2008 is 2 to 3 times larger than those under Franklin Roosevelt in the mid-Thirties.

Despite 10-11 years of economic recovery and a near-record low unemployment rate, the US budget deficit under president Trump is similar to the level seen in the mid-Thirties. On top of that, Trump and his administration have no intention whatsoever to change their expansionary fiscal policy and reduce the huge budget deficit, which is in fact projected to worsen further.

An important reason for the persistence of America’s budget deficit, even during prolonged economic recoveries, is the country’s aggressive defence spending. Many people blame the US deficits on entitlement programmes even though they are not supported by the Budget. Total US defence spending will amount to more than US$1 trillion in fiscal year 2020, with US military spending alone making up 73% of that massive sum. US military spending is greater than the next 10 largest government expenditures combined. It is four times greater than China's military budget. It is very difficult to reduce the US budget deficit without cutting her defence spending. Another reason is the impact of tax cuts, not just during president Bush’s time but also under Trump, and yet another key item is the unfunded elements of US mandatory spending. These refer not to Social Security but part of Medicare and Medicaid. Only Acts of Congress can change the mandatory spending. That would require a majority vote in both houses and is thus unlikely to happen.

"An important reason for the persistence of America’s budget deficit, even during prolonged economic recoveries, is the country’s aggressive defence spending."

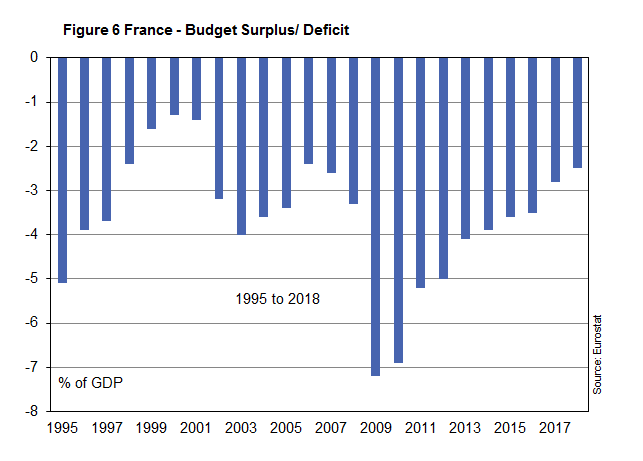

France has also been maintaining an expansionary fiscal policy, both pre and post 2008 (figure 6).

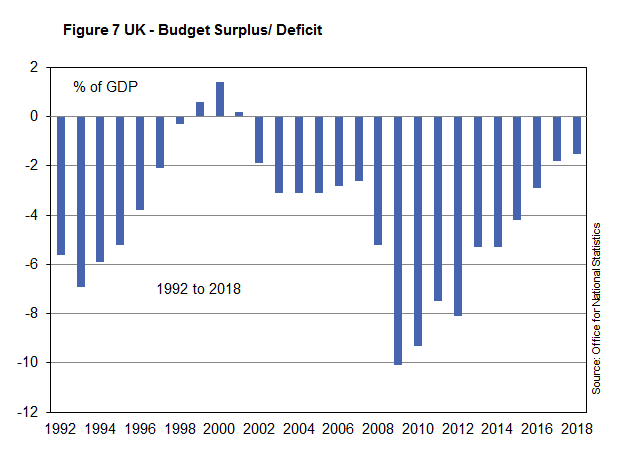

Like the other developed economies, the UK has also been maintaining an expansionary fiscal policy, both pre and post 2008 (figure 7).

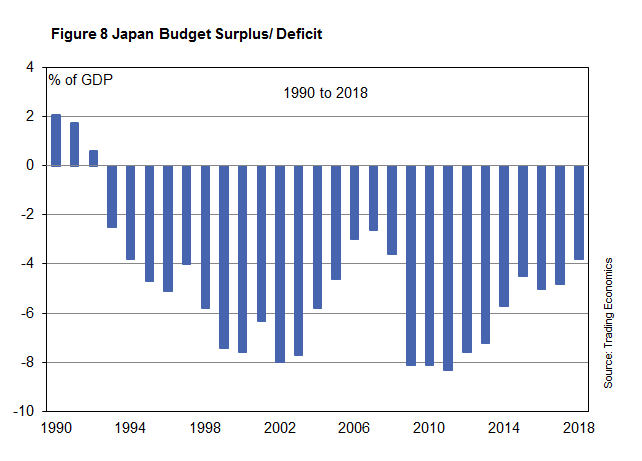

Japan, once upon a time the 2nd largest economy in the world, has been implementing an expansionary fiscal policy and bearing a very high budget deficit for a long time (figure 8). During the Great Depression, Japan resorted to military aggression by invading China and other Asian countries. This led to economic growth and hence Japan was able to enjoy nice budget surpluses. Nowadays, because Japan cannot adopt such a brutal policy of conquest, the economy has been suffering since the early Nineteen Nineties. Japan has been forced to resort to a futile expansionary fiscal policy and high budget deficit for decades.

"During the Great Depression, Japan resorted to military aggression by invading China and other Asian countries. This led to economic growth and hence Japan was able to enjoy nice budget surpluses."

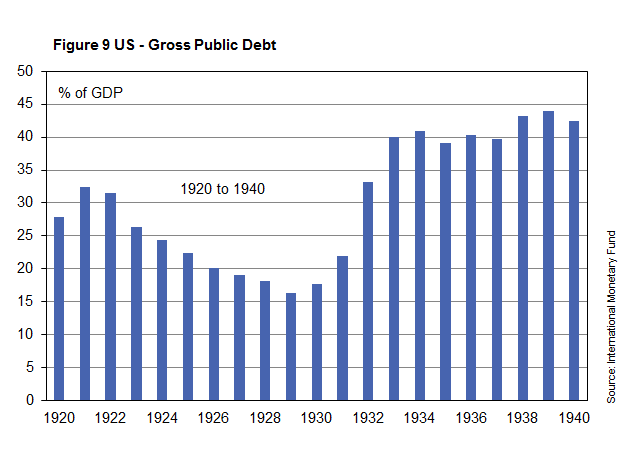

An expansionary fiscal policy and a persistent budget deficit lead to high public debt. The experience of the US and Japan is typical. Both countries have seen an explosion in government debt. In the period before and during the Great Depression, public debt in the US was low, especially before 1930 (figure 9). Remember that there was a budget surplus and a deficit only crept into the US economy in the mid-Thirties when fiscal policy had no choice but to become expansionary. In those times, public debt and government borrowing were seen as bad habits that should be avoided at all cost.

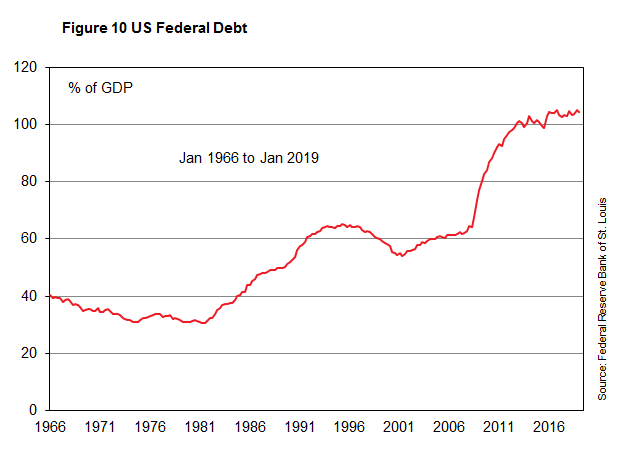

Nowadays, US public debt is a lot, lot higher than it was 80 or 90 years ago, especially after the US-created economic crisis in 2008 (figure 10). Nowadays, the thinking is the opposite. The government spends more, the government receives less, and the government borrows more. In this equation, it is crucial that US inflation does not rise further. When this happens, US interest rates would have to climb up. And when interest rates rise, all hell will break loose for the US economy, which already suffers from a high and persistent budget deficit and high and rising government debts.

"Nowadays, the thinking is the opposite. The government spends more, the government receives less, and the government borrows more. In this equation, it is crucial that US inflation does not rise further"

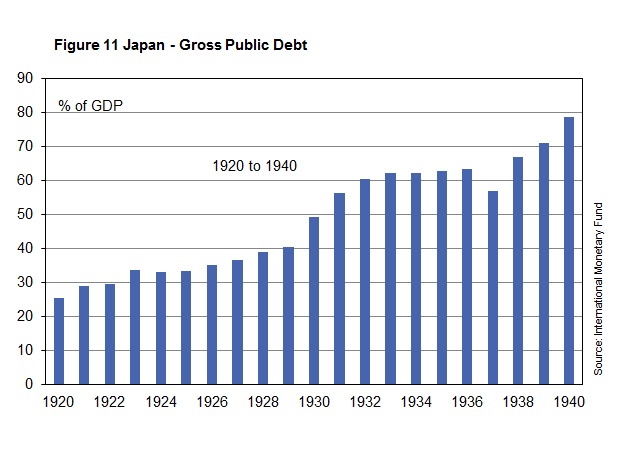

In the period surrounding the Great Depression, Japan’s public debt followed a pattern similar to that of the US (figure 11). In the case of Japan, public debt rose as that particularly nasty Asian country went round invading other Asian countries.

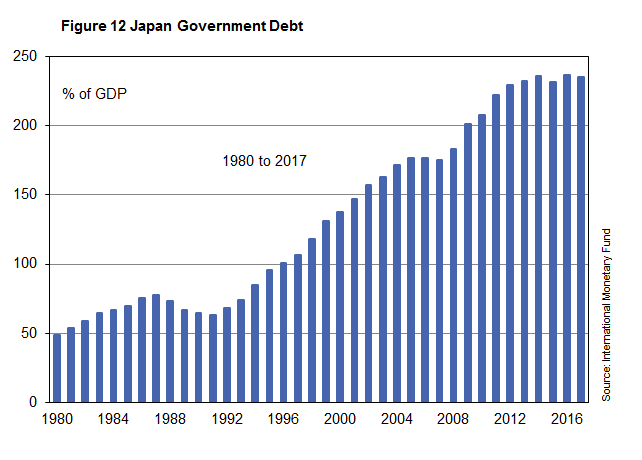

Again, in a manner most similar to the US and other developed economies, Japan has implemented the same policy of “Government spends more, government receives less, and the government borrows more”. Because Japan’s economic mess started earlier than the US or Europe, Japan now has the rare honour of bearing the highest government debt in the whole world (figure 12).

In the good old days, a prolonged low US unemployment rate, an extended ultra-loose monetary policy, a protracted expansionary fiscal policy and a persistent budget deficit would have led to a rising US inflation rate. Now, US bond yields are plunging and the financial markets are expecting more US rate cuts. It is remarkable how so much has changed, especially with regards to economic policies of the developed economies.

No debt or as little of it as possible, limited government spending, and a small role for the government were the economic orthodoxy before the US-led 1930 Great Depression and, to a lesser extent, before the US-led 2008 global financial crisis. Nowadays, the opposite is generally true - the mantra of more government intervention and more government spending is the main economic thinking. In a fundamental way, the US, Japan, UK and Europe are becoming more like China in the sense that the role of government is steadily increasing in these supposed free market economies. Let there be another economic crisis and we might see these countries becoming even more socialist than China.

"In a fundamental way, the US, Japan, UK and Europe are becoming more like China in the sense that the role of government is steadily increasing in these supposed free market economies. Let there be another economic crisis and we might see these countries becoming even more socialist than China."

Thanks to the protracted expansionary fiscal policy and almost perpetual budget deficit, the high public debt in Japan, most European countries and the United States will continue to climb. A “What, Me Worry ?” attitude prevails. This brings us to Germany and China, two major economies that stand apart from the other major ones.

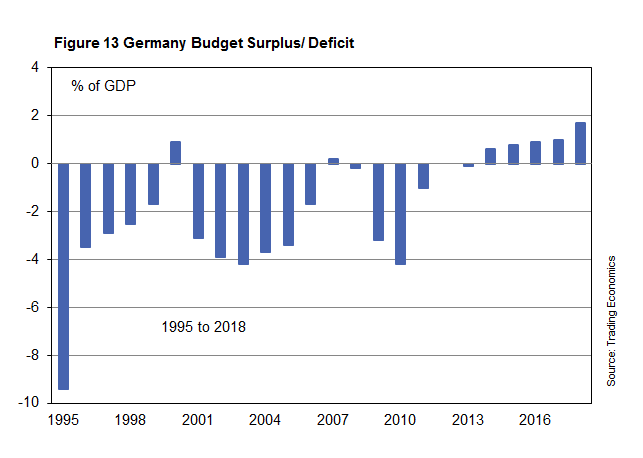

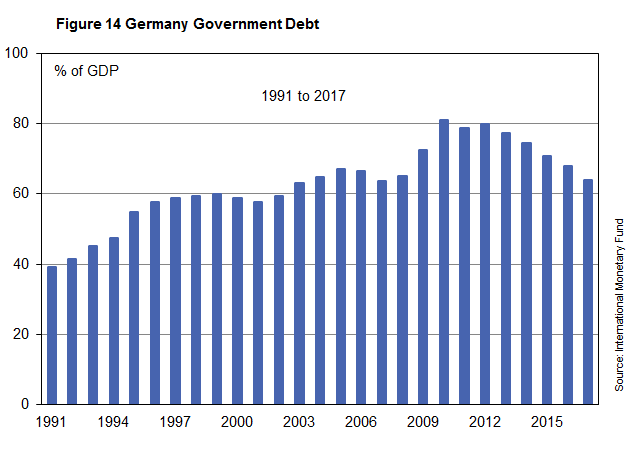

Germany was reunified in 1990 when East Germany became part of West Germany to form the reunited nation of Germany, and when Berlin reunited into a single city. This reunification was financially very costly but Germany made sure that her budget deficit did not grow out of control. Even after the 2008 US-led crisis, Germany enjoyed decent economic growth, thanks to her excellent economic relationship with China. Unlike the other developed economies, Germany soon began to enjoy budget surplus (figure 13), a remarkable economic achievement.

As a result, Germany’s government debt peaked out in 2010/2011 and has since then been falling steadily (figure 14). Few economies have been able to achieve this performance, especially in the context of the global environment after 2008 and a Europe that has been ripped apart by crisis after crisis.

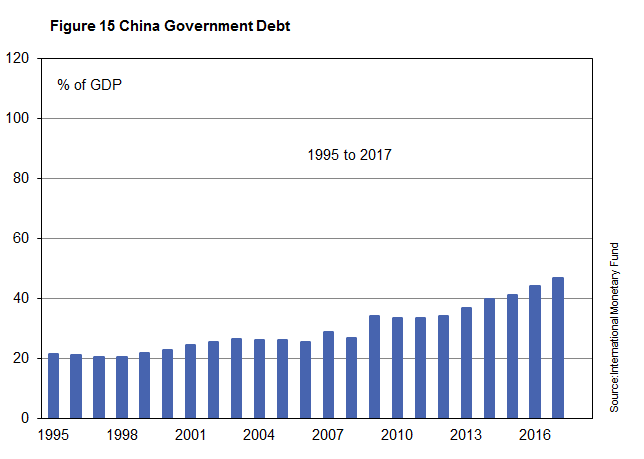

On the other side of the world, China has also been delivering an admirable economic performance. Although government debt has risen, it has done so from a very low base and, despite the increase, still stands at a healthy level (figure 15). While the US debt is above 100% of her GDP (and still rising), China’s government debt is less than half of that.

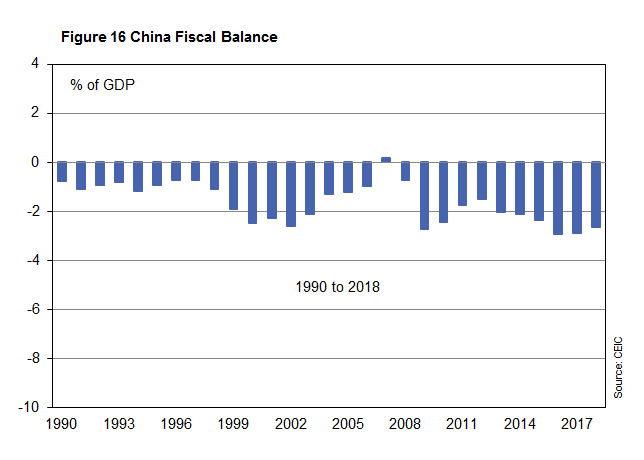

China has been experiencing budget deficit too (figure 16). Given her huge sustained public investment spending of all types, the deficit is not surprising. What has been outstanding is the fact that China’s budget defcit has remained at a low and healthy level for so long.

Monetary policy since the US-led 2008 global financial crisis has fundamentally changed. Fiscal policy since the 1930 Great Depression has also gone through similar. The next global recession will ensure that they remain the same for a very long time to come. What tools will be available to us then ?

At the beginning of this analysis, we wrote about how amazing it is that so much has stayed the same since i Capital was started in 1989. We also observed that it is no less amazing that so much has fundamentally changed. We have been asking ourselves if we are all living in a different world. In the coming issues of Volume 31, we will continue to reflect on the state of the nation and the state of the world as we explore disruptions and technological changes, and changes in investing, economy and society.

THE KLSE

As Malaysians get ready for Merdeka Day (31st Aug) and Malaysia Day (16th Sept), the nation remains more divided than before. This is not surprising – Malaysia will remain so as long as the country is under a leader whose main aim is to promote the supremacy of one race over other Malaysians.

"As Malaysians get ready for Merdeka Day (31st Aug) and Malaysia Day (16th Sept), the nation remains more divided than before. This is not surprising – Malaysia will remain so as long as the country is under a leader whose main aim is to promote the supremacy of one race over other Malaysians."

A recent Facebook post showing a man setting fire to the Malaysian flag ignited strong emotions in the country, with angry responses from the Malay community. Malaysian Chinese were accused of burning the symbol of the country’s sovereignty. Other users called the Chinese “pigs” and told them to leave the country.

Except the man in the picture was not Malaysian Chinese, and the photo was taken in 2013. According to media reports, a reverse Google image search showed it was of a retired Filipino policeman burning a Malaysian flag in Manila to protest against the handling of the Sabah issue by the then Philippines president Aquino.

Over the Causeway, we see a totally different portrayal of civilised social behaviour. What do we expect a Singaporean to look like ? A misunderstanding in a hawker centre escalated into an argument and eventually the realisation of what makes one Singaporean. Watch this short video from Project RED by the Singapore government and understand why one country is progressing happily with unity and why another country is sadly backsliding under the wrong leaders.

On 17 Aug 2019, we received the following unsolicited email from a subscriber, Jeff Chew (we produced the translated version below):

To Mr. Tan Teng Boo and your team,

I am a loyal reader of your i Capital publication and also shareholder of icapital.biz Bhd.

Introduced by a friend, I subscribed i Capital 5 years ago.

I’m writing to extend my gratitude to you and your team as the National Day of Malaysia approaches.

It really has helped me a lot to read i Capital.

It's not only about investing, but also about what's happening in the world right now, for better or worse.

I was particularly struck by the 90-year-old returning to the throne of prime minister with the government reshuffle on May 9.

i Capital has always been an independent, intelligent and truthful insight into Malaysia, and its coverage on Malaysia really brings back a lot of memories.

These reports, especially "Old Crooks, New Crooks, Regular Crooks" and "A horse & A Mathematician", make me marvel at the profound insights of I Capital today, which has been one year since May 9.

I suppose that you must be a rational and patriotic citizen, if not a prophet.

Last but not least, I wish Mr. Tan Teng Boo good health.

The world can do without heroes, but Malaysia cannot do without Tan Teng Boo.

As for the road ahead of Malaysia, in spite of all the difficulties, I would like to say, "if there are no difficulties, there will be no success."

A Malaysian Citizen

For Malaysians, as 31st Aug and 16th Sep approaches again, what is there to look to forward to ? On 29 Aug 2019, Malaysiakini bears this headline - “PM: No one wants to resign, so no room for Anwar in cabinet now.” Well, we all know who should resign. As i Capital has continuously warned, Malaysia faces a fluid and uncertain political landscape for the next 5 to 10 years. Based on Malaysia‘s political developments after the 2018 general election, we are even more convinced now that the next 5 to 10 years will be a difficult but crucial phase for Malaysia’s development. i Capital is retaining its long-term outlook as highly uncertain.

i Capital retains its immediate-term outlook of the KLCI at a range of 1,500 to 1,650 and repeats its warning that the KLCI risks plunging further. See Stop Press for the latest. i Capital retains its bearish short-term outlook at a range of 1,300 to 1,500. The bearish medium-term outlook of i Capital is preserved with a target of 700/800.